Speculating on vacancy decontrol

Sorry it's been forever. New year, new NYC mayor, exciting times to be getting back to writing about housing. Also I finally have my very own ✨chart aesthetic✨ so get ready, dear nerds.

As New York City approaches a rent freeze, people continue to be up in arms about the unsustainable cost burdens faced by landlords.

The thing about the distress in the rent stabilized market is that much of the cost being paid by current landlords is going to debt service, and that debt service was inflated due to speculation on vacancy decontrol prior to 2019.

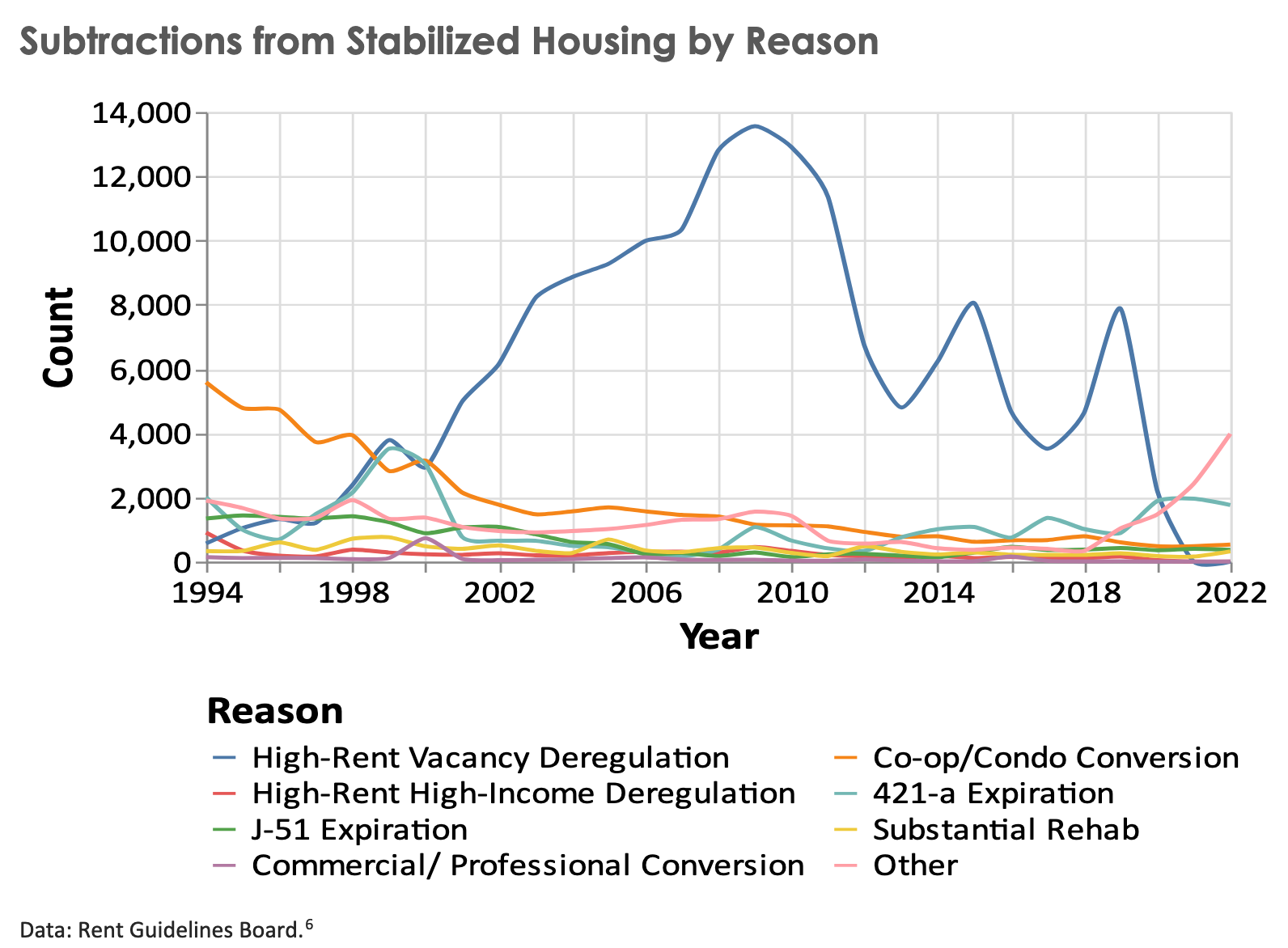

As a little background: until 2019, vacancy decontrol allowed landlords to remove units from rent stabilization if they could get rents above a certain threshold while the unit was vacant. The rent increases being regulated by the Rent Guidelines Board generally wouldn't allow rents to clear that threshold. But landlords were allowed to stack a few things that enabled rents to clear the threshold:

- A vacancy bonus of up to 20%

- Incentives that allowed rent increases based on improvements made to individual apartments (which were self-reported with little oversight)

- Incentives that allowed rent increases based on improvements to the building

Landlords used this extensively in the 2000s and 2010s to deregulate units.

(Nota bene, the chart above is from Brad Lander's paper where he puts to rest the myth that there are 20,000+ rent-stabilized units sitting vacant because repairs can't be afforded. There are few such units and broad support for improving maintenance incentives such as J-51.)

Buildings where vacancy decontrol was possible sold at a premium relative to other buildings. If we look at how many units were removed from rent control three years after the sale of each building, we see a clear relationship with the per-unit sale price of the building.

Buildings that lost more than 10% of their RS units after sale sold for a 46% premium over buildings without decontrols, in terms of price per unit medians.

It should be noted that this relationship breaks down when looking at buildings that had more than half of their units decontrolled. It's likely that extreme decontrol situations happen more in buildings that are distressed and small.

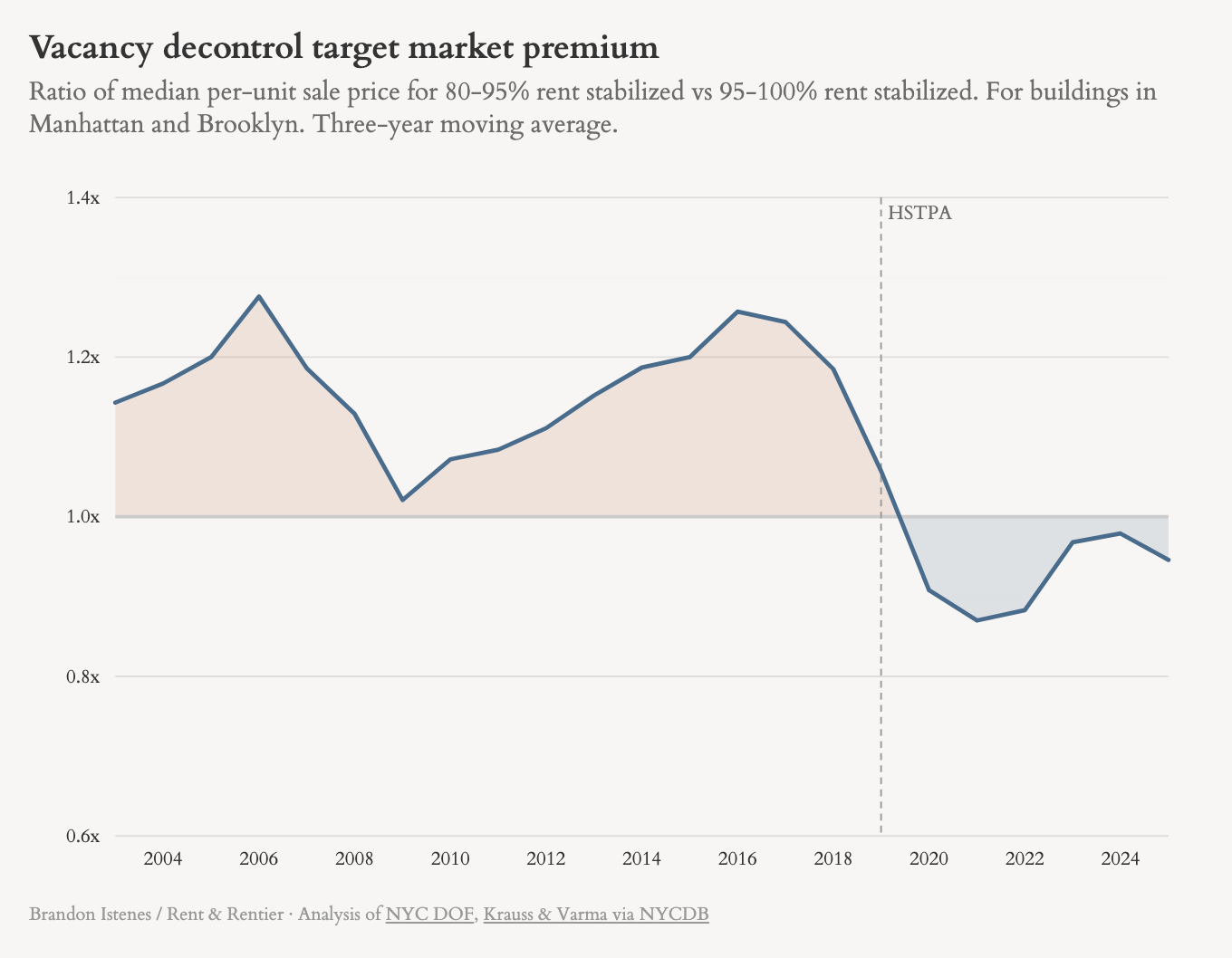

In 2019, the NY legislature passed the Housing Stability and Tenant Protection Act (HSTPA), the vacancy decontrol loophole was closed, and the price premium associated with it dried up. We can see this by looking at prices for the kinds of buildings that tended to be targeted for vacancy decontrol. Key factors determining whether a building was likely to have units deregulated 3 years after sale include:

- Rent stabilized unit share: Buildings with 80-95% RS units were much more likely to have decontrols (28.3% of such buildings) than buildings with 95-100% RS units (16.2%)

- Borough: Manhattan (23.2%) > Brooklyn (16.8%) > Queens (12.7%) > Bronx (3.7%)

So we'll look at a "decontrol target market" of 80-95% RS buildings in Manhattan and Brooklyn. A whopping 47.3% of these buildings lost RS within 3 years of sale. We'll compare that to 95-100% RS buildings in Manhattan and Brooklyn (because comparing across boroughs would introduce lots of confounding factors). In this control group, 29.7% of buildings lost units within 3 years of sale.

Both of these lines are affected by interest rates, cap rates, market conditions, and animal spirits. But the difference between them, I think, captures the vacancy decontrol premium. There's noise in the data, but it seems clear that the decontrol target market generally traded at a premium prior to HSTPA, and then that premium went away after.

Looking at the 3-year moving average of the ratio of these figures makes the picture even clearer. This chart shows the 80-95% prices divided by the 95-100% prices.

Prior to 2019, many buildings had been purchased at a price that assumed the buyer would be able to use vacancy decontrol to increase cash flow. Some of those buildings are now in crisis. This crisis was not caused by rent stabilization, but by speculation based on landlords exploiting a legal loophole that closed.

For buildings not yet in bankruptcy, many landlords are trying to keep paying their debts by foregoing maintenance. CPC (a major nonprofit lender) reported average maintenance expense for their RS portfolio decreased 10% from 2022 to 2023, despite an inflation rate of 8% in that year.

The sales of RS buildings at speculative prices transferred wealth from buyers to sellers, with buyers expecting to be able to extract a compensatory amount of wealth from renters. For the sellers it is a fait accompli. The current landlords are the ones left holding the bag. It is hard to feel too sorry for them, since their plight has been brought about by a grift they were actively participating in. But the distress of these buildings is a big problem for both them and for renters.

The best thing for tenants is intentional resolution of distressed buildings. Transition to social housing is the best path, and can be supported with COPA policies and social housing finance (such as revolving loan funds). But even receivership or sale is generally preferable to a deepening maintenance crisis. Landlords cannot be allowed to muddle along, deferring maintenance in hopes that a policy change might make them whole again. This is the case in NYC now, as it is in any municipality adopting rent stabilization. Cities and municipalities using rent stabilization have a responsibility to do two things:

- Enforce building codes and ensure resolution of distress

- Not flinch

If landlords believe that a policy change will salvage a deal that is presently underwater, they will wait it out, making their tenants' lives miserable in the meantime. A municipality adopting rent stabilization should not be caught flinching.

Here in Kingston, where I'm writing from, the adoption of rent stabilization through ETPA has faced both legal challenges as well as the opposition of the mayor. Flinch central. Landlords are holding on to buildings that they are underwater on, as one court case after another holds the system in limbo. Very few of the tenants that are owed back-rent have received it. Maintenance isn't happening, not because landlords don't have the money, but because they don't want to invest in buildings that might be worth 40% less than they had bargained for.

Vacancy decontrol is not the whole story

While the vacancy decontrol premium is an important part of the history of rent-stabilized building prices, it's not the whole story. Something is happening in parts of the rent-stabilized market where decontrol was a minor feature:

You can take the wiggles of the unregulated market to give a sense of the baseline market fluctuations, interest rates and all that. NYC-wide, rent-stabilized buildings are trading at Great Recession level multiples. And the trend from 2024 to 2025 looks pretty concerning.

Side note, these multiples I'm using come from the median rents by regulation status, which I have collected from the Housing and Vacancy Survey:

When we break it down by borough, however, the picture seems less worrying. Median sale values are toward the low end of historical normal, but a substantial part of that is the deflation of a Manhattan-based bubble from 2019-2021. The reason for this bubble is a mystery to me but I would be interested to hear if anyone has ideas.

This might be a troubled market for a while. To ensure that tenants don't suffer for it, NYC will need to provide both strong building enforcement and encourage resolution of distressed properties. Good, decisive governance is needed to protect tenants during these transition periods—even when the transition is a move toward greater tenant protections.